|

|

|

|

|

|

|

|

|

|

|

|

| Course Dates |

| Contact Us |

Financial Markets Glossary

A - C

| 30/360: | (Or 360/360). A day/year count convention assuming 30 days in each calendar month and a 'year' of 360 days; Sometimes adjusted for certain periods ending on 31st day of the month or the last day of February | |

| 360/360: | Same as 30/360. |

|

| Acceptor: | The person who accepts liability for a bill of exchange. | |

| Accreting: | An accreting principal is one which increases during the life of the deal. See amortising, bullet. |

|

| Accrued interest: | The proportion of interest or coupon earned on an investment from the previous coupon payment date until the value date. |

|

| Accumulated value: | Same as future value. |

|

| ACT/360: | A day/year count convention taking the number of calendar days in a period and a 'year' of 360 days. |

|

| ACT/365: | (Or ACT/365 fixed). A day/year count convention taking the number of calendar days in a period and a 'year' of 365 days. Under the ISDA definitions used for interest rate swap documentation, 'ACT/365' means the same as ACT/ACT. |

|

| ACT/365 fixed: | See ACT/365. |

|

| ACT/ACT: | A day/year count convention taking the number of calendar days in a period and a 'year' equal to the number of days in the current coupon period multiplied by the coupon frequency. For an interest rate swap, that part of the interest period falling in a leap year is divided by 366 and the remainder is divided by 365. |

|

| Adjustable peg: | Management of a currency at a fixed exchange rate against another currency or basket of currencies, with ad hoc adjustments to that fixed rate. See crawling peg. |

|

| Allocated account: | Ownership of specific gold bars held in a specific location and allocated to the holder’s account. See unallocated account. |

|

| American: | An American option is one which may be exercised at any time during its life. See European. |

|

| Amortising: | An amortising principal is one which decreases during the life of the deal, or is repaid in stages during a loan. Amortising an amount over a period of time also means accruing for it pro rata over the period. See accreting, bullet. |

|

| Annuity: | An investment providing a series of (generally equal) future cashflows. |

|

| Appreciation: | An increase in the market value of a currency in terms of other currencies. See depreciation, revaluation. |

|

| Arbitrage: | Arbitrage is the simultaneous operation in two or more different but related markets in order to take advantage of a discrepancy between them which will lock in a profit. The arbitrage operation itself usually tends to cause the different markets to move back in line. Covered interest arbitrage involves either the lending and borrowing of a currency in different centres, or the creation of a borrowing in one currency by borrowing another and converting the currency borrowed by means of a foreign exchange swap deal to produce the required currency at a cheaper rate. |

|

| Around par | (Or A/P). A foreign exchange swap price is around par if the left side is negative and the right side is positive. |

|

| Asian: | An Asian option depends on the average value of the underlying over the option's life. |

|

| Ask: | See offer. |

|

| Asset swap: | An interest rate swap or currency swap used in conjunction with an underlying asset such as a bond investment. See liability swap. |

|

| Asset-backed security: | A security which is collateralised by specific assets - such as mortgages - rather than by the intangible creditworthiness of the issuer. |

|

| ATM: | See at-the-money. |

|

| At-the-money: | (Or ATM). An option is at-the-money if the current value of the underlying (this often means the current forward value, rather than the current spot value) is the same as the strike price. See in-the-money, out-of-the-money. |

|

| BA: | See bankers’ acceptance. |

|

| Back office: | The operational department of the bank. |

|

| Backtesting: | Testing a model, such as a VaR model, against historic data. |

|

| Backwardation: | The situation when a forward or futures price for something is lower than the spot price (the same as forward discount in foreign exchange). See contango. |

|

| Baht: | A weight measurement for gold (0.47 troy ounces = 14.6 grammes), used in Thailand. |

|

| Balance sheet exposure: | See translation exposure. |

|

| Band: |

|

|

| Banker's acceptance: | See bill of exchange. |

|

| Banking book: | For the purposes of capital adequacy, that part of a bank's business which broadly involves its lending department and long-term investments. |

|

| Barrier option: | A barrier option is one which ceases to exist, or starts to exist, if the underlying reaches a certain barrier level. See knock out / in. |

|

| Base currency: | Exchange rates are quoted in terms of the number of units of one currency (the variable or counter or quoted currency) which corresponds to one unit of the other currency (the base currency). |

|

| Basis: | The underlying cash market price minus the futures price. In the case of a bond futures contract, the futures price must be multiplied by the conversion factor for the cash bond in question. |

|

| Basis point: | In interest rate quotations, 0.01% |

|

| Basis risk: | The risk that the prices of two instruments will not move exactly in line - for example the price of a particular bond and the price of a futures contract being used to hedge a position in that bond. |

|

| Basis swap: | An interest rate swap where both legs are based on floating rate payments. |

|

| Basis trade: |

|

|

| BBA: | British Bankers’ Association. (See www.BBA.org.uk). | |

| Bear spread: | A spread position taken with the expectation of a fall in value in the underlying. |

|

| Bearer security: | A security where ownership for the purpose of paying coupons and principal is determined by whoever is physically in possession of the security. There is no central record of ownership; this provides anonymity to investors. See registered security. |

|

| Bid: | In general, the price at which the dealer quoting a price is prepared to buy or borrow. The bid price of a foreign exchange quotation is the rate at which the dealer will buy the base currency and sell the variable currency. The bid rate in a deposit quotation is the interest rate at which the dealer will borrow the currency involved. The bid rate in a repo is the interest rate at which the dealer will borrow the collateral and lend the cash. See offer. |

|

| Big figure: | In a foreign exchange quotation, the exchange rate omitting the last two decimal places. For example, when EUR/USD is 1.2510 / 20, the big figure is 1.25. See points. |

|

| Bilateral netting: | Settlement netting between two parties. See multilateral netting. |

|

| Bilateral repo: | A repo with only two parties involved, the seller (lender of securities) delivering the securities to the buyer (lender of cash) rather than to a third party. See triparty repo, hold-in-custody. |

|

| Bill of exchange: | A short-term zero-coupon debt issued by a company to finance commercial trading. If it is guaranteed by a bank, it becomes a banker's acceptance. |

|

| Binomial tree: | A mathematical model to value options, based on the assumption that the value of the underlying can either move up or move down in given way over a given short time. This process is repeated many times to give a large number of possible paths (the 'tree') which the value could follow during the option's life. |

|

| BIS: |

|

|

| Black-Scholes: | A widely used option pricing formula devised by Fischer Black and Myron Scholes. |

|

| Bond basis: | An interest rate is quoted on a bond basis if it is on an ACT/365, ACT/ACT or 30/360 basis. In the short term (for accrued interest for example), these three are different. Over a whole (non-leap) year however, they all equate to 1. In general, the expression 'bond basis' does not distinguish between them and is calculated as ACT/365. See money-market basis. |

|

| Bond-equivalent yield: | The yield which would be quoted on a US treasury bond which is trading at par and which has the same economic return and maturity as a given treasury bill. |

|

| Bono: | Bono del Estado, a Spanish government fixed-coupon bond. |

|

| Bootstrapping: | Building up successive zero-coupon yields from a combination of coupon-bearing yields. |

|

| Bräss/Fangmeyer: | A method for calculating the yield of a bond similar to the Moosmüller method but, in the case of bonds which pay coupons more frequently than annually, using a mixture of annual and less than annual compounding. |

|

| Break forward: | A product equivalent to a straightforward option, but structured as a forward deal at an off-market rate which can be reversed at a penalty rate. |

|

| Broken date: | (Or odd date) A maturity date other than the standard ones (such as 1 week, 1, 2, 3, 6 and 12 months) normally quoted. |

|

| BTAN: | Bon du Trésor à Taux Fixe et Interêt Annuel, a French government bond. |

|

| BTF: | Bon du Trésor à Taux Fixe et Interêt Précompté, a French government discount bill. |

|

| BTP: | Buono del Tesoro Poliennale, an Italian Treasury bond. |

|

| Bull spread: | A spread position taken with the expectation of a rise in value in the underlying. |

|

| Bullet: | A loan / deposit has a bullet maturity if the principal is all repaid at maturity. See amortising. |

|

| Bullion: | Gold and silver traded in bulk form. |

|

| Bund: | Bundesanleihe, a German government bond. |

|

| Buy / sell-back: | Opposite of sell / buy-back. |

|

| Cable: | The exchange rate for sterling against the US dollar. |

|

| CAD: | ||

| Calendar spread: | The simultaneous purchase / sale of a futures contract for one date and the sale / purchase of a similar futures contract for a different date. See spread. |

|

| Call: | A call option is an option to purchase the commodity or instrument underlying the option. See put. |

|

| Cap: | Effectively equivalent to a series of borrower's IRGs, designed to protect a borrower against rising interest rates on each of a series of dates. |

|

| Capital adequacy directives: | (Or CAD). The various directives from the EU which together set out the capital adequacy rules. |

|

| Capital adequacy: | The concept that if some of a bank’s risks are realised, the bank should still have adequate capital to remain in business. |

|

| Capital market: | Long-term market (generally longer than one year) for financial instruments. See money market. | |

| Cash: | See cash market. |

|

| Cash market: | The market for trading an underlying financial instrument, where the whole value of the instrument will potentially be settled on the normal delivery date - as opposed to contracts for differences, futures, options etc. (where the cash amount to be settled is not intended to be the full value of the underlying) or forwards (where delivery is for a later date than normal). See derivative. |

|

| Cash-and-carry: | A round trip (arbitrage) where a dealer buys bonds, repos them out for cash to fund their purchase, sells bond futures and delivers the bonds to the futures buyer at maturity of the futures contract. |

|

| CCT: | Certificato di Credito del Tesoro, an Italian Treasury credit certificate. |

|

| CD: | ||

| Ceiling: | Same as cap. |

|

| Certificate of deposit: | (Or CD) A security, generally coupon-bearing, issued by a bank to borrow money. |

|

| CHAPS: | Clearing House Automated Payments System, the UK payments clearing system. |

|

| Charting: | See technical analysis. |

|

| Cheapest to deliver: | (Or CTD) In a bond futures contract, the one underlying bond amongst all those which are deliverable, which is the most price-efficient for the seller to deliver. | |

| Cherry picking: | Insistence by a defaulting organisation on consummating profitable deals with a particular counterparty, while defaulting on unprofitable ones. |

|

| (Or CME). A futures exchange in Chicago. | ||

| Choice: | A choice price is one with a zero spread - i.e., the bid and offer are the same. |

|

| Classic repo: | (Or repo or US-style repo). Repo is short for 'sale and repurchase agreement' - a simultaneous spot sale and forward purchase of a security, equivalent to borrowing money against a loan of collateral. A reverse repo is the opposite. The terminology is usually applied from the perspective of the repo dealer. For example, when a central bank does repos, it is lending cash (the repo dealer is borrowing cash from the central bank). |

|

| Clean deposit: | Same as time deposit. |

|

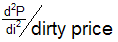

| Clean price: | The price of a bond excluding accrued coupon. The price quoted in the market for a bond is generally a clean price rather than a dirty price. |

|

| Close out and repricing: | When a repo is marked-to-market and the value of the collateral is found to have changed, the parties may either adjust the nominal amount of the collateral accordingly or terminate the repo early and re-establish it at the original repo rate but reflecting the new market price for the collateral. The latter is 'close out and repricing'. |

|

| Close-out netting: | See netting. |

|

| CLS: | ||

| CME: | ||

| Collar: | The simultaneous purchase of a call option and purchase of a put option at different strikes - typically both out-of-the-money - or the reverse. In interest rates, the simultaneous purchase of a cap and sale of a floor. |

|

| Collateral: | (Or security). Something of value, often of good creditworthiness such as a government bond, given temporarily to a counterparty to enhance a party's creditworthiness. In a repo, the collateral is actually sold temporarily by one party to the other rather than merely lodged with it. Also given by the borrower to the lender in a securities lending transaction. See general collateral and special collateral. |

|

| Commercial paper: | A short-term security issued by a company or bank, generally with a zero coupon. |

|

| Competitive exposure: | Economic exposure which arises specifically because of a competitor. |

|

| Compound interest | When some interest on an investment is paid before maturity and the investor can reinvest it to earn interest on interest, the interest is said to be compounded. Compounding generally assumes that the reinvestment rate is the same as the original rate. See simple interest. |

|

| Contango: | The situation when a forward or futures price for something is higher than the spot price (the same as forward premium in foreign exchange). See backwardation. |

|

| Continuous compounding: | A mathematical, rather than practical, concept of compound interest where the period of compounding is infinitesimally small. |

|

| Continuous linked settlement: | (Or CLS). A real-time PvP clearing system for settlement of FX transactions, where a payment from Bank A to Bank B is made only if, and at the same time as, the corresponding payment from Bank B to Bank A is made. | |

| Contract date: | The date on which a transaction is negotiated. See value date. |

|

| Contract for differences: | A deal such as an FRA and some futures contracts, where the instrument or commodity effectively bought or sold cannot be delivered; instead, a cash gain or loss is taken by comparing the price dealt with the market price, or an index, at maturity. |

|

| Convenience yield: | The perceived benefit of holding a commodity, expressed as an interest rate per year. |

|

| Conversion factor: | (Or price factor). In a bond futures contract, a factor to make each deliverable bond comparable with the contract's notional bond specification. Defined as the price of one unit of the deliverable bond required to make its yield equal the notional coupon. The price paid for a bond on delivery is the futures settlement price times the conversion factor. |

|

| Convertible currency: | A currency that may be freely exchanged for other currencies. |

|

| Convexity: | A measure of the curvature of a bond's price / yield curve (mathematically, |

|

| Correlation coefficient: | A measure of the extent to which two things do, or do not, move together. |

|

| Corridor: | The purchase of a cap combined with the sale of a cap at a higher strike. |

|

| Cost of carry: | The net running cost of holding a position (which may be negative) - for example the cost of borrowing cash to buy a bond less the coupon earned on the bond while holding it. |

|

| Counter currency: | See variable currency. |

|

| Counterparty risk: | The risk that a counterparty might default on a contract by failing to pay amounts due or failing to fulfil the delivery conditions of the contract. |

|

| Coupon: | The interest payment(s) made by the issuer of a security to the holders, based on the coupon rate and face value. |

|

| Coupon swap: | An interest rate swap in which one leg is fixed-rate and the other is floating -rate. See basis swap. |

|

| Covariance: | A measure of the extent to which two things do, or do not, move together. |

|

| Cover: | To cover an exposure is to deal in such a way as to remove the risk - either reversing the position, or hedging it by dealing in an instrument with a similar but opposite risk profile. |

|

| Covered call / put: | The sale of a covered call option is when the option writer also owns the underlying. If the underlying rises in value so that the option is exercised, the writer is protected by his position in the underlying. Covered puts are defined analogously. See naked. |

|

| Covered interest arbitrage: | Creating a loan / deposit in one currency by combining a loan / deposit in another with a forward foreign exchange swap. |

|

| CP: | See commercial paper. |

|

| Crawling peg: | Management of a currency at a fixed exchange rate against another currency or basket of currencies, with a regular pre-determined adjustment to that fixed rate. See adjustable peg. |

|

| Credit risk: | The risk that a counterparty defaults on a transaction or that the issuer of a security defaults on coupon or interest payments. |

|

| Cross: | See cross-rate. |

|

| Cross-currency repo: | A repo in which the currency of the cash is different from the currency in which the collateral is denominated. | |

| Cross-rate: | Historically, an exchange rate between two currencies, neither of which is the US dollar. Nowadays, any exchange rate calculated from two or more existing rates. | |

| CT: | Certificat du Trésor, Belgian Treasury bill. |

|

| CTD: | ||

| CTO: | Buono del Tesoro con Opzione, Italian Treasury certificate with an option. | |

| Cum-dividend: | When (as is usual) the next coupon or other payment due on a security is paid to the buyer of a security. See ex-dividend. |

|

| Cumulative probability distribution: | The probability that any one of a series of numbers will be no greater than a particular number. |

|

| Currency swap: | An agreement to exchange a series of cashflows determined in one currency, possibly with reference to a particular fixed or floating interest payment schedule, for a series of cashflows based in a different currency. See interest rate swap. |

|

| Current yield: | Bond coupon as a proportion of clean price per 100; does not take principal gain / loss or time value of money into account. See yield to maturity, simple yield to maturity. |

|

| Customer repo: | When the US Federal Reserve ('Fed') does a repo with the market on behalf of one of its own customers, such as another central bank or supranational organisation. See Fed repo, system repo. |

|

| Cylinder: | Same as collar. |

|

Markets International Ltd

Aylworth, Naunton

Cheltenham GL54 3AH

e-mail: ask@markets-international.com

home | training | course dates | elearning | glossary | books | contact us

).

).