|

|

|

|

|

|

|

|

|

|

|

|

| Course Dates |

| Contact Us |

Financial Markets Glossary

I - N

| Icing: | To ice a security is to reserve it (generally for a fee) for another party who may wish to borrow it in future. |

| ICMA: | The International Capital Markets Association (formerly ISMA, and before that the AIBD), the international professional body governing dealing in securities. See SIFMA . |

| ICOM: | International Currency Options Market standard documentation for netting foreign exchange option settlements. |

| IFEMA: | International Foreign Exchange Master Agreement, a master agreement for foreign exchange spot and forward deals. |

| IMM: | The International Monetary Market, the financial division of the Chicago Mercantile Exchange, the futures market in Chicago. |

| Immunisation: | The construction of a portfolio of securities so as not to be adversely affected by yield changes, provided it is held until a specific time. |

| Implied repo rate: | The break-even interest rate at which it is possible to sell a bond futures contract, buy a deliverable bond, and repo the bond out. See cash-and-carry. |

| Implied volatility: | The volatility used by a dealer to calculate an option price; conversely, the volatility implied by the price actually quoted. |

| Index swap: | Sometimes the same as a basis swap. Otherwise a swap like an interest rate swap where payments on one or both of the legs are based on the value of an index - such as an equity index for example. |

| Indexed repo rate: | Where the repo rate in a classic repo is periodically re-set with reference to some benchmark such as LIBOR. |

| Indirect: | An exchange rate quotation against the US dollar in which the dollar is the base currency and the other currency is the variable currency. |

| Initial margin: | See margin. |

| Integration: | The third stage of money laundering, in which the money is reinvested in the legitimate economy. See placement, layering. |

| Interbank: | An interbank transaction is one between two banks, as opposed to one between a bank and an end-user. |

| Interest rate guarantee: | |

| Interest rate swap: | (Or IRS). An agreement to exchange a series of cashflows determined in one currency, based on fixed or floating interest payments on an agreed notional principal, for a series of cashflows based in the same currency but on a different interest rate. May be combined with a currency swap. |

| Internal rate of return: | (Or IRR). The yield necessary to discount a series of cashflows to an NPV of zero. |

| International Monetary Market | The financial sector of the Chicago Mercantile Exchange. |

| Interpolation: | The process of estimating a price or rate for value on a particular date by comparing the prices actually quoted for value dates either side. See extrapolation. |

| Intervention: | Purchases or sales of currencies in the market by central banks in an attempt to reduce exchange rate fluctuations or to maintain the value of a currency within a particular band, or at a particular level. Similarly, central bank operations in the money markets to maintain interest rates at a certain level. |

| In-the-money: | A call (put) option is in-the-money if the underlying is currently more (less) valuable than the strike price. (For a European option, typically considers the underlying’s current forward price rather than it’s current spot price). See at-the-money, out-of-the-money. |

| Inverted yield curve | See negative yield curve. |

| IRG: | |

| IRR: | |

| IRS: | See interest rate swap. |

| ISDA master agreement: | International Swaps and Derivatives Association master agreement for FRAs, swaps, options and other transactions. |

| ISDA: | International Swaps and Derivatives Association, the professional association for swaps dealers and authors of ISDA documentation, used for a range of derivatives deals. |

| ISLA: | International Securities Lenders' Association. |

| ISO: | International Standards Organisation. |

| Iteration: | The repetitive mathematical process of estimating the answer to a problem, by trying how well this estimate fits the data, adjusting the estimate appropriately and trying again, until the fit is acceptably close. Used for example in calculating a bond's yield from its price. |

| JGB: | Japanese government bond. |

| Judgmental analysis: | See fundamental analysis. |

| Kappa (k): | Same as vega. |

| Knock out / in: | A knock out (in) option ceases to exist (starts to exist) if the underlying reaches a certain trigger level. See barrier option. |

| Lambda (l): | Same as vega |

| Large exposure risk: | The requirement to allocate more capital for capital adequacy purposes if the total exposure to any one counterparty is a particularly large proportion of the bank’s total. |

| Layering: | The second stage of money laundering, in which the money is passed through a series of transactions to obscure its origin. See placement, integration. |

| LBMA: | London Bullion Market Association, the trade association for the physical gold and silver markets. |

| Lease rate: | (Or ‘gold LIBOR’). The interest rate borne by gold. |

| Legacy currency: | (Or national currency unit). One of the former national currencies which became a unit of the euro. |

| Legal risk: | The risk that the bank’s business is affected by changes in laws and regulations, or by existing laws and regulations which it had not properly taken into account. |

| Letter repo: | Same as hold-in-custody repo. |

| Liability swap: | An interest rate swap or currency swap used in conjunction with an underlying liability such as a borrowing. See asset swap. |

| LIBID: | See LIBOR. |

| LIBOR: | London inter-bank offered rate, the rate at which banks are willing to lend to other banks of top creditworthiness. The term is used both generally to mean the interest rate at any time, and specifically to mean the rate at a particular time (often 11:00 a.m.) for the purpose of providing a benchmark to fix an interest payment such as on an FRN. LIBID is similarly London inter-bank bid rate. LIMEAN is the average between LIBID and LIBOR. |

| LIFFE: | London International Financial Futures and Options Exchange. |

| Lift: | To lift an offer is to deal on the offered price quoted by someone. |

| LIMEAN: | See LIBOR. |

| Limit up / down: | Futures prices are generally not allowed to change by more than a specified total amount in a specified time, in order to control risk in very volatile conditions. The maximum movements permitted are referred to as limit up and limit down. |

| Liquid | A liquid market is one where it is easy to find buyers and sellers at good prices. A liquid investment is one which can easily be turned into cash because there is a liquid market in that instrument. |

| Liquidity | See liquid. |

| Liquidity risk: | The risk of being unable to find a liquid market for a particular instrument. |

| Locals | Private traders on a futures exchange dealing for their own account. |

| Location swaps: | An exchange of gold (or other commodity) to be delivered in one location for delivery in another location. |

| Loco: | The physical delivery point for gold - e.g. ‘loco London’ means delivery in London. |

| Lognormal: | A variable's probability distribution is lognormal if the logarithm of the variable has a normal distribution. |

| Long: | A long position is a surplus of purchases over sales of a given currency or asset, or a situation which naturally gives rise to an organisation benefiting from a strengthening of that currency or asset. To a money market dealer however, a long position is a surplus of borrowings taken in over money lent out, (which gives rise to a benefit if that interest rate rises). See short. |

| Macaulay duration: | See duration. |

| Managed floating: | Same as dirty floating. |

| Manufactured dividend: | When a coupon is paid on collateral during the term of a classic repo, it is received by the buyer but repaid to the seller. The repayment is called a manufactured dividend. |

| Mapping: | In the variance / covariance approach to VaR, the process of representing a position in terms of other standardised instruments. |

| Margin: | In general, margin is typically collateral placed by one party with a counterparty at the time of a deal, against the possibility that the market price will move against the first party, thereby leaving the counterparty with a credit risk. In a repo, initial margin (or 'haircut') is the extra collateral or cash required to allow for a potential subsequent change in the collateral's market value. Usually required by the buyer to protect against a fall in the collateral's market value, but sometimes required by the seller to protect against a rise in the collateral's market value. Variation margin is a payment made, or collateral transferred, subsequently from one party to the other in order to adjust the amount of collateral because the market price has moved. In repo for example, variation , the amount of cash or collateral which must be transferred when there is a change in the value of the collateral, in order to bring the ratio between the values of cash and collateral back to that required under the repo agreement. In gilt repos, variation margin refers to the fluctuation band or threshold within which the existing collateral's value may vary before further cash or collateral needs to be transferred. In futures, initial margin is collateral placed at the beginning of the transaction; variation margin payment is subsequent settlement of profit / loss. In a loan, margin is the extra interest above a benchmark (e.g. a margin of 0.5% over LIBOR) required by a lender to compensate for the credit risk of that particular borrower. |

| Margin call: | A call by one party in a transaction for variation margin to be transferred by the other. |

| Margin ratio: | (As defined in the GMRA) the all-in market value of the securities divided by the cash loan, so that if the haircut is 2%, the margin ratio is 1.02. |

| Margin transfer: | The payment of a margin call. |

| Market risk: | The risk that the value of a position falls due to changes in market rates or prices. |

| Mark-to-market: | Generally, the process of revaluing a position at current market rates. |

| Matched book trading: | Offering two-way prices in repos. Does not imply that the dealer doing so in fact has a matched, or square, trading book. |

| Matched sale-purchase: | Same as a Fed reverse. |

| Mean: | Average. |

| Mine: | “I buy the base currency”. For example, if someone who has asked for and received a price says “5 mine!”, he means “I buy 5 million units of the base currency”. See yours. |

| Model risk: | The risk that the computer model used by a bank for valuation or risk assessment is incorrect or misinterpreted. |

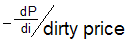

| Modified duration: | A measure of the proportional change in the price of a bond or other series of cashflows, relative to a change in yield. (Mathematically, |

| Modified following: | The convention that if a value date in the future falls on a non-business day, the value date will be moved to the next following business day, unless this moves the value date to the next month, in which case the value date is moved back to the last previous business day. |

| Money laundering: | The process of passing the proceeds of criminal activities through the financial system in order to disguise its criminal origins. |

| Money market: | Short-term market (generally up to one year) for financial instruments. See capital market. |

| Money-market basis: | An interest rate quoted on an ACT/360 basis is said to be on a money-market basis. See bond basis. |

| Monte Carlo simulation: | A method of calculating VaR by generating a very large number of random prices, applying these to the current portfolio of instruments and measuring the net effect. See historic VaR, variance / covariance. |

| Moosmüller: | A method for calculating the yield of a bond. |

| Multilateral netting: | Settlement netting between more than two parties. See bilateral netting. |

| My risk: | If someone who has asked for a price says “my risk”, he is acknowledging that the price may change before he has accepted it. |

| Naked: | A naked option position is one not protected by an offsetting position in the underlying. See covered call / put. |

| National currency unit: | See legacy currency. |

| NDF: | |

| Negative skewness: | A greater probability of a large downward movement than of a large upward movement. |

| Negative yield curve | (Or inverted yield curve) A downward-sloping yield curve. See positive yield curve. |

| Negotiable: | A security which can be bought and sold in a secondary market is negotiable. |

| Net exposure: | (As defined in the GMRA) the net total of: the transaction exposures on all outstanding deals, the net margin paid or received on all outstanding deals, and any manufactured payments which are due but not yet paid or received. This calculation gives the amount of margin transfer which may be called for. |

| Net margin: | (As defined in the GMRA) the amount of variation margin paid (including margin securities, margin cash and accrued interest on margin cash) from one party to the other, netted against the amount of variation margin paid or repaid in the other direction. |

| Net present value: | (Or NPV). The net present value of a series of cashflows is the sum of the present values of each cashflow (some or all of which may be negative). |

| Net-paying securities: | Securities where coupons are paid net of withholding tax. See gross-paying securities. |

| Netting: | Obligation netting is the payment, in the normal course of business, of one net amount from one party to another instead of a gross payment in each direction. Close-out netting allows, in the event of a default, the non-defaulting party to terminate all outstanding transactions and settle them with a single net payment or receipt. |

| Nominal amount: | Same as face value of a security. |

| Nominal rate: | A rate of interest as quoted, rather than the effective rate to which it is equivalent. |

| Non-deliverable forward: | Foreign exchange forward outright deal traded as a contract for differences. Instead of delivering one currently and receiving the other, the rate dealt is compared with the spot rate at maturity and the difference only is settled, usually in the base currency. |

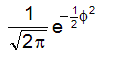

| Normal: | A normal probability distribution is a particular distribution assumed to prevail in a wide variety of circumstances, including the financial markets. Mathematically, it corresponds to the probability density function, |

| Normal probability function: | A particular probability density, with the formula |

| Normal yield curve | (Or positive yield curve) An upward-sloping yield curve. See negative yield curve. |

| Nostro: | A bank's nostro account is its currency account held at another bank. See vostro. |

| Notional: | In a bond futures contract, the bond bought or sold is a standardised non-existent notional bond, as opposed to the actual bonds which are deliverable at maturity. Contracts for differences also require a notional principal amount on which settlement can be calculated. |

| NPV: | See net present value. |

Markets International Ltd

Aylworth, Naunton

Cheltenham GL54 3AH

e-mail: ask@markets-international.com

home | training | course dates | elearning | glossary | books | contact us

). See

). See